A great deal has been written and discussed about the move toward passive investment. A recent Bloomberg article written by Barry Ritholtz quoted Bill Miller, legendary US stock picker, as saying the shift is not really from active management to passive but from expensive passive investment management to inexpensive passive management. Miller suggests about 70% of active managers are really closet indexers, even though they charge high fees.

“Worldly wisdom teaches that it is better for a reputation to fail conventionally than to succeed unconventionally”

…John Maynard Keynes

A great deal has been written and discussed about the move toward passive investment. A recent Bloomberg article written by Barry Ritholtz quoted Bill Miller, legendary US stock picker, as saying the shift is not really from active management to passive but from expensive passive investment management to inexpensive passive management. Miller suggests about 70% of active managers are really closet indexers, even though they charge high fees.

In our monthly commentaries over the past few years, we have written extensively on closet indexers or what other’s refer to as “herding”. This type of approach is employed to ensure a manager does not deviate too far from the index he or she is measured against, thereby ensuring their job is not at risk.

Laurus, up until now, has not had the advantage of backing up our claim to be a superior stock‐picker with any significant statistical evidence – we’ve just not been around long enough. However, with the team from Bluewater Investment Management officially joining Laurus at the end of September, along with their extensive track record, we’re afforded the opportunity to illustrate how great stock‐pickers add value for their clientele.

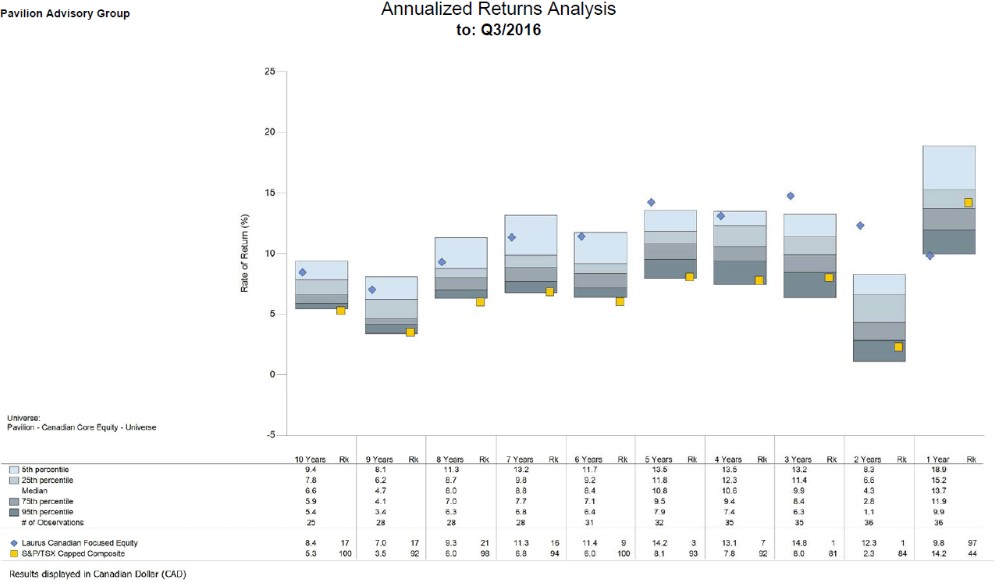

With acknowledgement to Pavilion Advisory Group for the illustration, the chart included above shows the past ten years of representative Bluewater returns relative to the Canadian equity peer universe. At first glance, one notices that annualized performance results all group across the upper levels of peer manager returns (except the current year ‐ a result of many managers pursuing short term commodity stock performance). In the detail, one can see the consistency of absolute results, with even the past year providing investors with an absolute return of 10%.

Behind this performance lies very interesting statistics. The current 93% “active share” (a measure of the percentage of stock holdings in a managers portfolio that differ from the benchmark index) is very high when compared to the TSX Composite. The five year tracking error (standard deviation of excess returns to the benchmark) is also very high, as is the Sharpe ratio and Jensen Alpha (measures of risk‐ adjusted return).

All of these factors indicate a skilled portfolio manager holding great investments for his clients. With his low turnover rate, and superb fundamental portfolio statistics (weighted return on equity of 24%, 13% free cash flow margin, 14% return on capital), the conviction level on underlying holdings is clearly in evidence.

Which is why we’re so very excited to have Dennis Starritt join Laurus. His investment style is analogous to that of our current investment process, and his investment acumen is without parallel. Our team is very fortunate to have Dennis join us.

While true that passive investing is continuing to attract many investors, we suggest Mr. Miller may be quite correct – the movement is away from the closet indexers. Dennis has ensured his clients have had the benefit of superb stock picking over a very long time frame.