“The thing I find most interesting about investing is how paradoxical it is: how often the things that seem most obvious—on which everyone agrees—turn out not to be true.”

…Howard Marks

One of the most misunderstood investment allocations in Canada is Canadian equity. Over the past few years, institutional investors have been reducing their Canadian equity allocations to minimize “home country bias”. A June 2014 article by Russell Investments reported the average pension plan had 18% of their total assets allocated to Canadian equity which represented 41% of their total traditional equity exposure. Additionally, institutional investors are being advised to incorporate a defensive strategy in Canadian equity to de‐risk and better manage portfolio risk to provide resilience in down markets to ensure return outcomes are aligned with investor expectations.

This advice is likely due to our considerable commodity bias in the underlying Canadian indices, which has increased volatility and impairs long term returns through cyclicality.

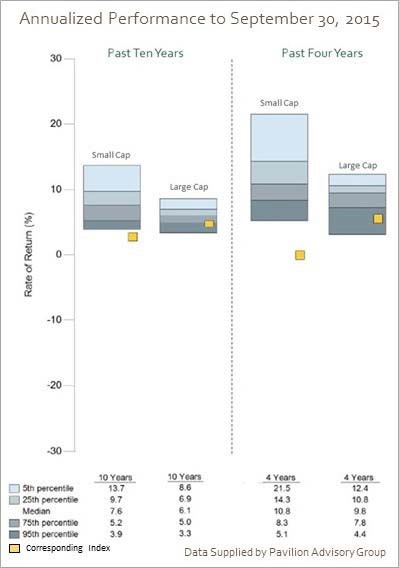

But very little thought has being given to return outcomes WITHIN the Canadian equity investment class. With thanks to Pavilion Advisory Group in Montreal, our chart illustrates that institutional managers biased to large capitalization stocks do not add any significant value to the overall TSX Composite index (“Index”) over the past four years. In fact, as the chart also illustrates, over longer periods (ten years) the performance differential between the highest and lowest investment manager return compresses – over a four year period the spread from top to bottom is 8% but narrows to 5% over ten years.

It’s a very different experience with institutional small cap investing. Over the four year period, the better managers generated a return 16% higher than the lowest manager performance. This spread only narrows to 10% over ten years. And over both periods, ALL managers outperformed the TSX Small Cap Index.

Furthermore, over both periods virtually ALL small cap institutional managers outperformed the broader TSX Composite Index. And over both periods, more than 30% of small cap managers outperformed the very best large cap managers.

One could argue this data represents only a specific period. However, looking back over time at selected Pavilion data, it appears the patterns remain constant.

Therefore, any decision made to invest in Canadian equities, must also include an allocation to high quality small cap portfolios to generate consistent performance gains with lower volatility.

Some might also argue that a large cap manager could add performance by sprinkling the portfolio with a few small cap stocks. While this might enhance performance, investing in small cap stocks requires expertise and experience that large cap managers lack. And the Pavilion data shows that merely adding a few small caps does not match the benefits of a dedicated small cap allocation.

All great businesses in today’s large cap market began as small companies, yet investors continue to allocate only a small sliver of their portfolio to small cap investing. This is likely due to a combination of lack of familiarity and the perception of higher risk. It is much easier for investors to relate to the merits of holding a Royal Bank or a Loblaws than a small, unfamiliar small cap company. Similarly, it’s much easier to conceive of smaller, less‐familiar names as having greater risk of business failure.

Statistics show that the volatility associated with a high quality small cap portfolio is no greater than that of a large cap portfolio. The reward, however, is significant. The greater inefficiencies in the small cap market, along with their ability to generate higher cash flow and earnings growth (the principal drivers of long‐term stock performance) than more mature companies, will ensure consistent outperformance to large caps over a cycle. We urge investors to consider increasing their allocation to smaller capitalization investing.